- A Guide to Tria and KAST Crypto Debit Cards

- What Is a Crypto Debit Card?

- Why Is This Especially Useful in Southeast Asia?

- Two Popular Options: Tria and KAST

- Tria — Around per Year with Up to 6% Cashback

- Real-Life Spending Simulation (Philippines Example)

- KAST — Free Card Issuance

- Which One Should You Choose?

- How Do You Use It in Grocery Stores?

- Important: This Is Not an Investment Strategy

- Summary

A Guide to Tria and KAST Crypto Debit Cards

In the previous article, we explained how OFWs (Overseas Filipino Workers) and migrant workers in Southeast Asia can send USDT home at lower cost.

But an important question comes next:

How can your family actually use the USDT they receive?

Many people assume:

“Don’t we still need to convert it to cash first?”

The good news is — not anymore.

Today, your family can spend crypto directly in daily life using a crypto debit card.

What Is a Crypto Debit Card?

A crypto debit card allows you to:

Spend cryptocurrency at VISA or Mastercard merchants, just like a regular debit or credit card.

You can use the crypto card by adding to your smartphones like this.

Here’s how it works:

- Connect your crypto wallet to the card

- Pay at supermarkets, restaurants, or online stores

- The crypto is automatically converted to local currency at checkout

That means:

✔ No bank account required

✔ No ATM withdrawals needed

✔ No extra currency exchange steps

Your family can simply use the card as usual.

Why Is This Especially Useful in Southeast Asia?

In many Southeast Asian countries:

- Large parts of the population are underbanked

- Many families rely on overseas remittances

- Smartphone usage is high

A crypto debit card simplifies the process from:

Send → Convert to Cash → Pay

to simply:

Send → Spend

This is not just convenience — it reduces friction and unnecessary fees in everyday life.

Two Popular Options: Tria and KAST

Two crypto debit card providers gaining attention are:

- Tria

- KAST

Each has a different value proposition.

Tria — Around per Year with Up to 6% Cashback

Tria requires purchasing the card.

For example:

- Virtual card: around $20 per year

- Higher-tier plans: $90+

At first glance, you might wonder why you should pay for a card.

The answer is cashback.

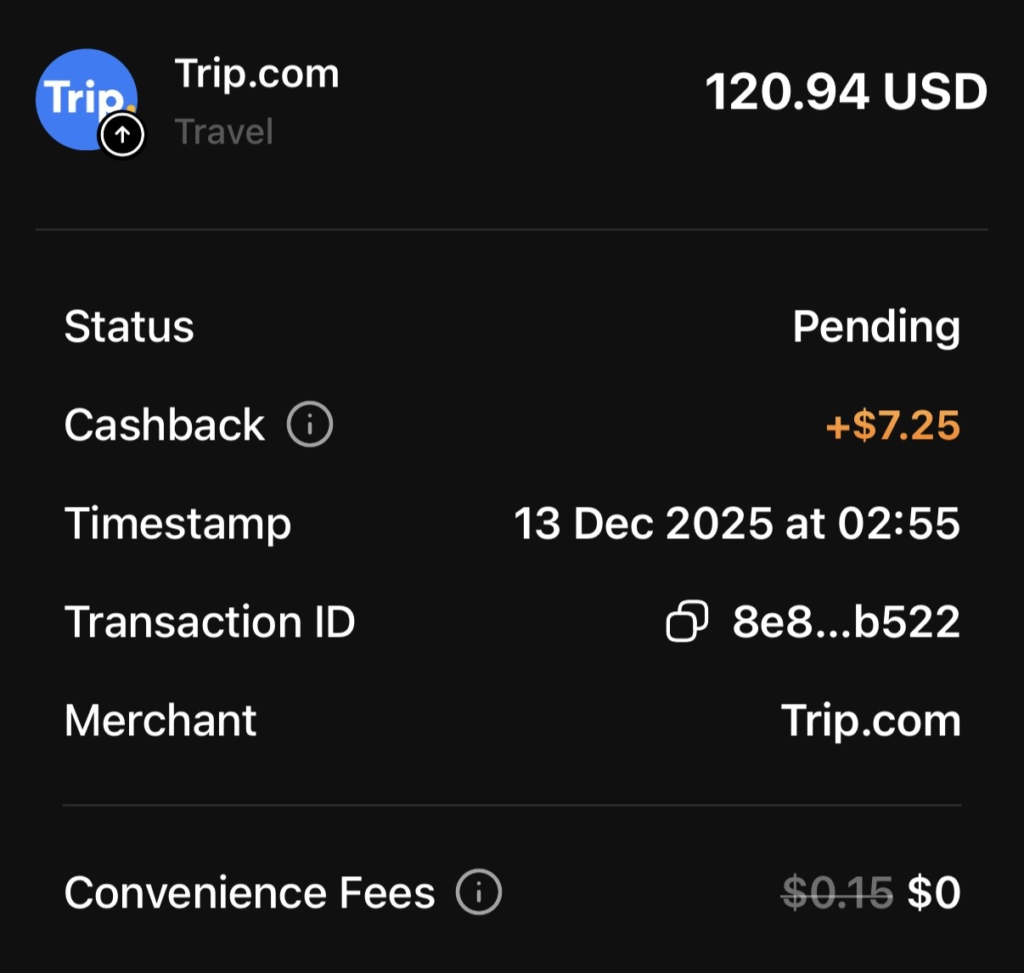

Up to 6% Cashback on Spending

Tria offers up to 6% cashback on eligible transactions.

Let’s look at a realistic example.

Tria Earn(Like Bank Saving)

Tria has a system similar to a bank savings account. If you’re not using your money for payments, you can deposit it into the Earn feature (which works like a bank deposit), and earn up to an 8% annual interest rate.

For example, if you deposit $1,000, you’ll earn $80 in a year. Regular bank savings accounts never offer this level of interest. (Note: The screenshot shows a base APY of 8% for USDC on Ethereum, with potential boosts up to 12% depending on membership tiers, badges, etc.)

Real-Life Spending Simulation (Philippines Example)

Monthly household expenses:

- Groceries: $300

- Utilities: $120

- School expenses: $150

- Transportation & mobile costs: $130

Total: $700 per month

With 6% cashback:

$700 × 6% = $42 per month

Annual cashback: $504

After subtracting the $20 annual fee:

👉 Net positive: $484 per year

That amount could cover nearly a full month of groceries.

For OFW families, this is not a small difference.

Tria Invitation Link

If you sign up using the link below, you may qualify for a 20% referral reward when inviting friends. (We’ll cover how to earn through referrals later in the article.)

http://app.tria.so

(Please check the official website for the latest terms and rewards.)

KAST — Free Card Issuance

KAST’s strength is simplicity.

✔ No card issuance fee

✔ No upfront cost

✔ Easy for beginners to test

If you prefer to start without paying any annual fee, KAST may be a comfortable option.

KAST Invitation Link

If you use the link below, you may also receive a 20% discount on higher-tier premium cards, subject to the provider’s terms.

https://go.kast.xyz

(Terms and availability may vary depending on your country.)

Which One Should You Choose?

| Situation | Recommended |

|---|---|

| Just want to try crypto payments | KAST |

| Planning to use monthly for family expenses | Tria |

| Higher monthly spending | Tria |

| Prefer zero upfront cost | KAST |

If your family spends $500–$1,000 per month, Tria’s cashback model may provide better long-term value.

How Do You Use It in Grocery Stores?

The process is simple:

- Present the card at checkout

- Tap or insert like a regular debit card

- Payment completes

Behind the scenes, USDT is automatically converted to local currency, and the store receives payment normally.

Your family doesn’t need to handle crypto manually.

You can use it for:

- Supermarkets

- Restaurants

- Utility payments

- Online shopping

In short:

Crypto can function just like everyday money.

Important: This Is Not an Investment Strategy

This is not about speculation.

It’s not about holding crypto hoping for price increases.

It’s about:

Sending money home and allowing your family to spend it efficiently.

Your hard-earned income deserves better efficiency.

Summary

Traditionally:

Send → Convert to Cash → Pay → Lose in Fees

Now:

Send → Spend Directly → Earn Cashback

Lower remittance costs + spending rewards can create meaningful yearly savings.

For OFW families, that difference can add up to hundreds of dollars per year.

In the next article, we’ll explain:

👉 How to earn rewards by referring friends

👉 How to become a crypto card ambassador and generate side income

Stay tuned.

コメント